For a lot of growing SaaS companies, spend starts getting messy long before finance tools catch up. One team is buying software with a card, another is pushing invoices through email, reimbursements are scattered, and nobody has a clean view of what the company is actually committing to every month. That is the kind of problem Airbase is built to solve. Today, the product sits inside Paylocity for Finance, which says it combines spend management with Paylocity’s broader platform so companies can manage payroll and non-payroll expenses with more visibility and control.

The short answer is yes, Airbase looks like a strong fit for many SaaS companies that want tighter control over spend. But it is the right fit for a specific kind of company. It makes the most sense for teams that are past the scrappy startup stage, have growing approval complexity, and need a better system for subscriptions, invoices, corporate cards, procurement, and accounting sync. It makes less sense if what you really want is a true banking platform with deposits, treasury, and lending at the center. The sources around Airbase consistently frame it as a software-first spend management and finance automation product, not a bank replacement.

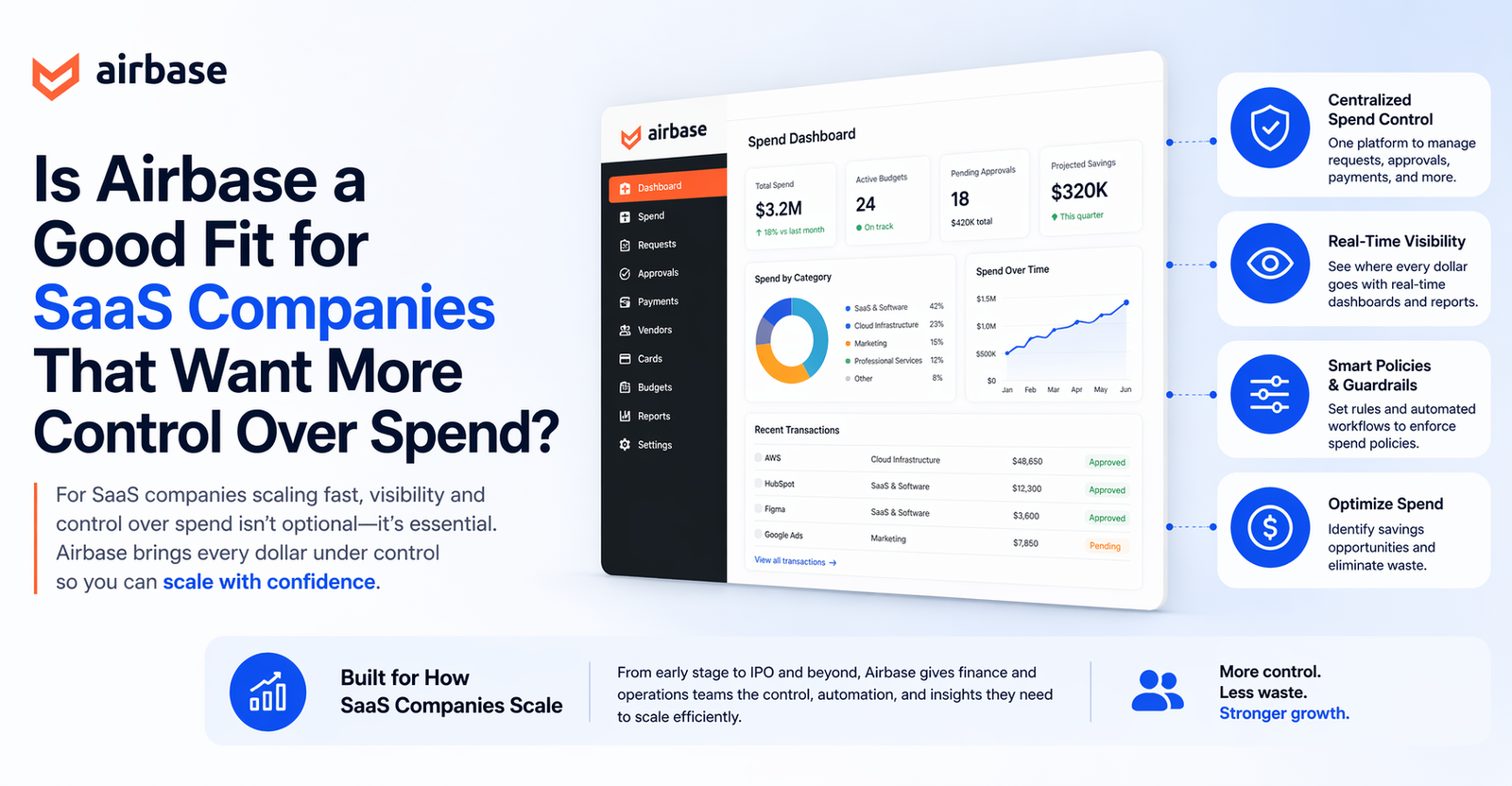

Where Airbase actually fits

One of the clearest things in the research is that Airbase is not best understood as “banking for SaaS companies.” It is better understood as a unified spend control layer. Paylocity describes the finance product around Expense Management, Corporate Cards, AP Automation, Guided Procurement, Spend Analytics, Policy Compliance, and Vendor Management. Contrary Research goes even further, calling Airbase a software-first platform that consolidates expense management, procurement, accounts payable, and corporate cards on one system.

That distinction matters because a lot of founders lump cards, reimbursements, AP, and banking into one mental bucket. Airbase sits close to banking activity, but that is not the same as being a banking platform. Contrary notes that customers who want to keep their existing card programs can integrate them through partnerships with American Express and Silicon Valley Bank, which reinforces the point that Airbase is designed to orchestrate spend workflows around existing financial infrastructure rather than replace everything underneath it.

Why it makes sense for growing SaaS teams

This is where Airbase starts to look especially practical for SaaS businesses. Workflow Automation’s review says one of the strongest use cases is Mid-Market SaaS Companies, especially teams with roughly 100 to 500 employees managing a growing pile of vendor subscriptions. The review says those companies benefit from virtual card controls and guided procurement, because each subscription can get its own card, cancellations are easier, and finance teams can see software spend in real time.

That fits a very common SaaS pain point. Subscription sprawl is not just a budgeting problem. It becomes a visibility problem, a policy problem, and eventually a finance-close problem. The same review repeatedly highlights use cases like virtual cards for SaaS subscriptions, AP automation for vendor invoices, and real-time budget tracking, which is exactly the kind of operating discipline growing software companies tend to need once spending becomes distributed across departments.

The product also looks well suited to companies that want to move from reactive spending to controlled spending. Contrary describes Guided Procurement as a module that directs employees to gather information from stakeholders like IT, procurement, and legal before purchases move forward, and says it can route requests into tools like Jira, Ironclad, and Slack. That matters in SaaS because spend often starts with software, contractors, or vendor tools, and those purchases tend to cross multiple teams before finance ever sees them.

The real strength is control, not just convenience

A lot of finance tools promise convenience. What stands out more in the Airbase story is control. The Recharge case study on Paylocity’s site says the company originally assumed it would need separate systems for credit cards, expense management, and bill pay, but instead used Airbase by Paylocity as one platform. The case study also says the finance team gained stronger visibility into departmental spend, saw a decrease in zombie spend and other unplanned expenses, and benefited from a NetSuite integration that helped shrink the monthly close from 25 to 30 days to less than a week.

That kind of outcome matters more than a feature list. For a SaaS company, better spend control is rarely just about seeing transactions. It is about reducing surprise spend, tightening approvals, and giving finance a cleaner path into the ERP and general ledger. If the case study is directionally representative, Airbase is strongest when it becomes part of the operating rhythm of the finance team, not just a place where cards get issued.

Where Airbase may fall short

Even if the fit is strong, it is not universal. The first limitation is category confusion. If a company is specifically looking for a banking-first product with deposits, treasury management, or broader cash-management tools, Airbase is probably not the clearest match. The public descriptions center on spend management, finance automation, AP, procurement, reimbursements, and cards, not bank-led infrastructure.

The second limitation is that Airbase appears to be more comfortable in the mid-market than at the very smallest or most heavily customized enterprise end. Contrary says Thejo Kote wanted to stay focused on companies with 200 to 2K employees, and also notes that this focus means trading off some functionality and customization that larger enterprise customers may demand. That suggests Airbase is strongest when a business has meaningful process complexity, but not so much complexity that it needs a deeply bespoke finance stack.

There is also a practical point around cards. Tipalti’s comparison page says Airbase deprecated its charge-card program and now only offers pre-funded cards. Because that page is competitor-authored, it should be read with some caution, but it is still a relevant signal that Airbase’s card setup may not look like a full banking-style credit product for every buyer. For some teams that will be perfectly fine. For others, especially those comparing it to more banking-adjacent fintech tools, it could matter.

So, is Airbase a good fit?

For the right SaaS company, yes. Airbase looks like a good fit for teams that want much tighter control over non-payroll spend, especially if they are juggling subscriptions, vendor invoices, employee expenses, approval chains, and ERP reconciliation. It seems particularly well suited to mid-market software businesses that have outgrown loose card programs and scattered AP workflows but are not looking for a full bank replacement.The clearest way to say it is this: Airbase is less of a banking product and more of a finance operations layer. If your goal is better visibility, stronger approvals, cleaner procurement, and tighter spend controls across a growing SaaS organization, it looks like a strong option. If your goal is true banking infrastructure, it is probably only part of the answer, not the whole thing.