If you are new to startup fundraising, the whole thing can feel confusing fast. People throw around terms like pre-seed, Series A, lead investor, venture capital, and private equity as if everyone already knows what they mean. In reality, most founders only learn the system by living through it. The good news is that the structure is not as complicated as it first looks. Most startups move through a fairly familiar sequence of funding rounds, and each stage tends to attract a different kind of investor.

At the simplest level, startup funding rounds are milestones. A company raises money, uses that capital to hit a new level of progress, and then raises again from investors who are comfortable with that next stage of risk. Early on, the story is usually about the idea, the team, and the first signs of product potential. Later, it becomes more about traction, revenue, market size, and the ability to scale. That is why the investors behind each round often change as the business grows.

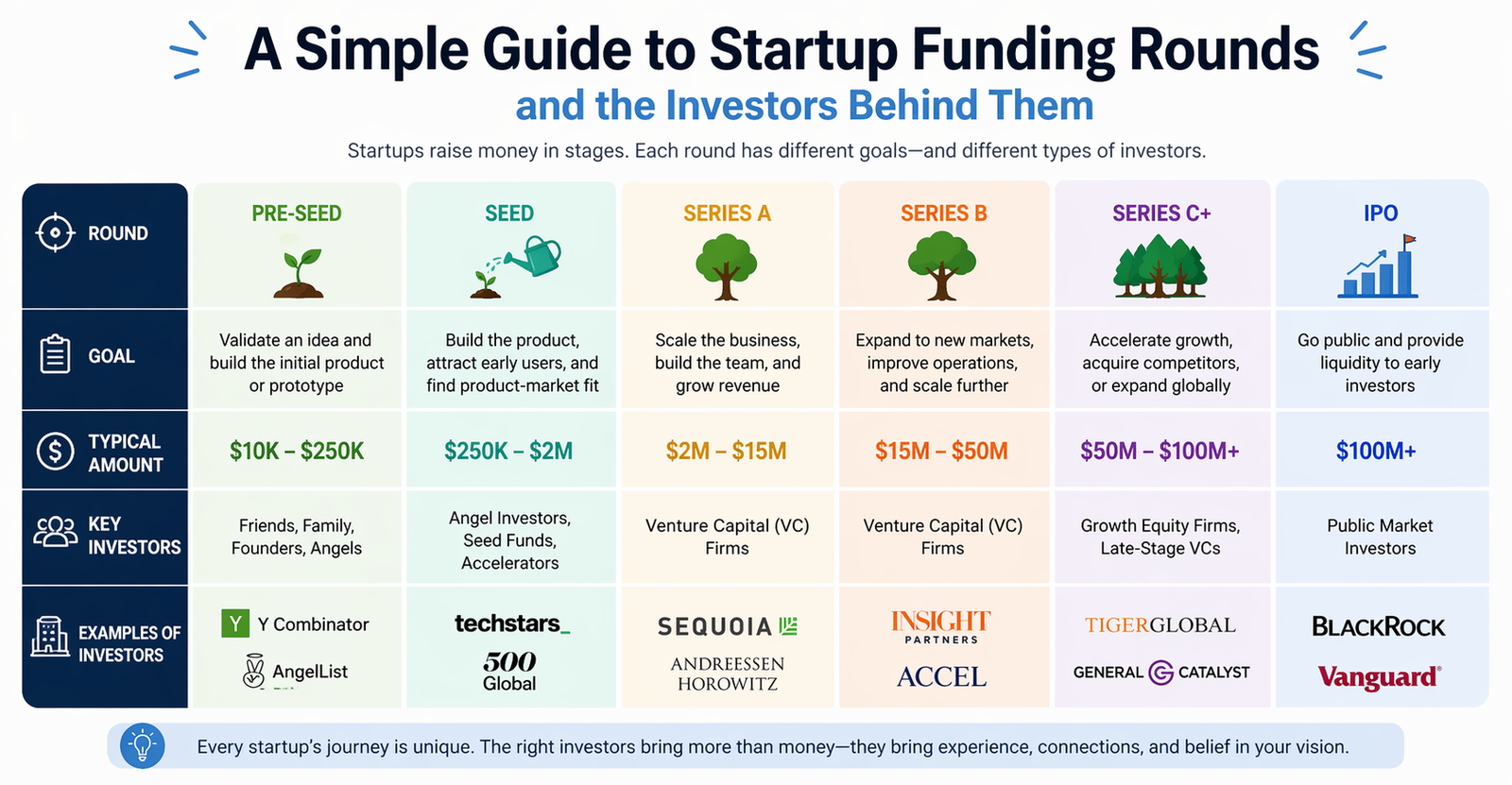

Why funding rounds exist in the first place

Most startups do not raise all the money they will ever need in one shot. They raise in steps because risk changes over time. A company at the idea stage is much riskier than a company with paying customers, and that company is riskier than one with strong revenue and international expansion plans. As risk goes down and proof goes up, founders can usually raise more money on better terms. Innoventure describes this well by explaining that startup financing often happens as a series of transactions, sometimes even in tranches, because the company matures over time while its capital needs increase.

This step-by-step system also helps investors. A friend who writes the first small check is taking a very different bet than a venture fund that joins at Series B. One is backing people and potential. The other is backing a company that should already have clearer market evidence. That is why understanding funding rounds is really about understanding how risk, proof, and investor expectations evolve together.

Pre-seed is where the journey usually starts

The pre-seed round is usually the earliest formal outside capital a startup raises. At this stage, the company may still be refining the idea, building an early version of the product, testing assumptions, or looking for its first signs of market demand. Ful.io describes pre-seed as the stage focused on idea development and proof of concept, while Innoventure links it to financing from friends and family, business angels, and very early investors.

The investors behind a pre-seed round are usually people comfortable with very high risk. That can include friends and family, angel investors, small seed funds, and occasionally early-stage venture capital firms that like to move early. These investors are not expecting polished financial systems or a mature sales engine. They want to see a credible founding team, a real problem worth solving, and enough potential to justify taking a chance before the business is fully formed.

For founders, this round is often less about maximizing valuation and more about getting enough capital to build something real. That may mean hiring early team members, finishing an MVP, talking to customers, and proving that the product deserves a larger next round.

Seed funding is where the company starts to look real

The seed round is often the first stage where the startup begins to look like a business instead of just a promising idea. By now, founders are usually expected to have a product in the market, early user feedback, and at least some traction that shows people care. Ful.io frames this stage around product development and early customer traction, while Plug and Play presents seed funding as the stage where startups move from concept toward business execution.

The investors here are often angel investors, dedicated seed funds, and early-stage VCs. Some of them will want to lead the round, while others will participate alongside a lead. At this point, investors are still taking a big leap, but they usually want more than a pitch deck. They want signs that the product solves a real problem and that the team can execute.

A good example from your SERP is Undefined Technologies. In 2021, citybiz reported that Undefined Technologies Corp completed a Seed Series round at a valuation just under $2 million, led by Dresden Capital Partners Fund, Ltd., with participation from Rio Vista Advisors, Inc., Biscayne Bay Advisors LLC, and Thunder Road Properties, L.P. The company was developing a quiet eVTOL cargo drone based on ion propulsion technology. That is a useful reminder that seed rounds are often about backing a strong concept, a technical vision, and a founder with a believable plan to turn early innovation into a real commercial business.

Series A is where investors want real proof

A lot of people think Series A is just a bigger seed round. It is not. This is usually the stage where investors want to see evidence that the company is finding product-market fit and building a repeatable business model. According to Ful.io, Series A is about product-market fit and business model validation. In plain English, that means the startup should be able to explain not only what it does, but why customers buy it, why they keep using it, and how the company plans to grow revenue in a reliable way.

The investors behind a Series A are usually more traditional venture capital firms. These firms still accept risk, but they want more structure. They will care about growth metrics, retention, customer feedback, early revenue quality, and whether the market is big enough to support a large company. They also start thinking more seriously about how the founding team scales into a leadership team.

This is where fundraising starts to feel less like storytelling and more like evidence. A founder may still need a strong vision, but numbers begin to matter a lot more.

Series B is about scaling what already works

By the time a company reaches Series B, the question is usually no longer “does this business make sense?” The question becomes “how big can this get?” Ful.io describes Series B as the stage for market expansion and operational scaling. That might mean building out sales, investing more heavily in marketing, entering new markets, strengthening the product, or improving the infrastructure needed to support a larger customer base.

The investors behind Series B rounds tend to be larger venture capital firms, along with existing investors who decide to follow on. These investors expect more maturity. They want to see a proven revenue model, clearer operational discipline, and enough momentum to justify a larger check. Innoventure also notes that more mature companies are typically less risky, which helps explain why larger funds often become more active as startups move into later rounds.

At this point, founders are not just being judged on possibility. They are being judged on execution.

Series C and later rounds are about expansion, dominance, or exit preparation

Once a startup reaches Series C and beyond, it is usually thinking on a bigger scale. Ful.io says these later rounds often support international growth, acquisitions, and large-scale expansion. Depending on the company, this stage can also be tied to preparing for an IPO, a strategic sale, or some other major liquidity event.

The investors behind these rounds can include late-stage venture funds, private equity, hedge funds, corporate investors, and earlier backers who continue to double down. The company at this stage is supposed to look much more like a mature operating business. Investors are studying metrics, margins, efficiency, leadership quality, and market position in much more detail.

A good late-stage contrast from your SERP is DeepWay. The Next Web reported that DeepWay completed $310 million in pre-IPO financing, with the latest tranche led by Stone Venture and participation from investors including NGS Super, Xiamen Guosheng Fund, ABC Impact, and Nanjing Ronghe Venture Capital. That is a very different investor profile from what you see in pre-seed or seed rounds. By then, the conversation is not about whether the company deserves to exist. It is about how much larger it can become and how close it may be to a public-market or strategic outcome.

What investors really look for at each stage

Even though the round names change, a few investor questions show up again and again. One helpful summary from a LinkedIn post by Patrick Henry breaks it down neatly: investors often pass because the startup is too early, because it is not solving a big enough problem in a large enough market with a strong enough value proposition, or because they do not have enough confidence in the team. That is informal commentary, but it matches how most funding decisions work in practice.

At the earliest stage, investors focus heavily on founders, vision, and market opportunity. At the middle stages, they want proof of traction and a repeatable business model. Later on, they care more about scale, efficiency, leadership depth, and whether the company can defend its position. The startup changes, and so does the investor mindset.

Why the right investor matters as much as the money

One mistake founders sometimes make is treating every investor like the same kind of partner. They are not. A great angel investor may be helpful for introductions and early conviction, but not equipped for later-stage scaling advice. A strong Series A VC may be excellent at helping with hiring and go-to-market strategy. A late-stage fund may care much more about financial discipline, expansion, and exit planning.

That is why the phrase “the investors behind them” matters so much in any discussion of funding rounds. The check is important, but the fit matters too. The best investors are not just writing money into the business. They are backing the company at the moment where their style, network, and expectations actually make sense.

How founders should think about the next round

The smartest way to approach startup funding is not to obsess over round labels. It is to ask a more practical question: what proof do I need to earn the next kind of investor? If you are pre-seed, that may mean proving customer interest. If you are seed, it may mean showing traction and a sharper product. If you are heading toward Series A or Series B, it usually means showing that growth is not random and that the business has real structure behind it.

That is what makes startup funding rounds easier to understand. They are not just names on a cap table. They are checkpoints in the life of a company. And the investors behind each round are really just different kinds of people making different kinds of bets at different levels of risk. Once you see that clearly, the fundraising path starts to make a lot more sense.