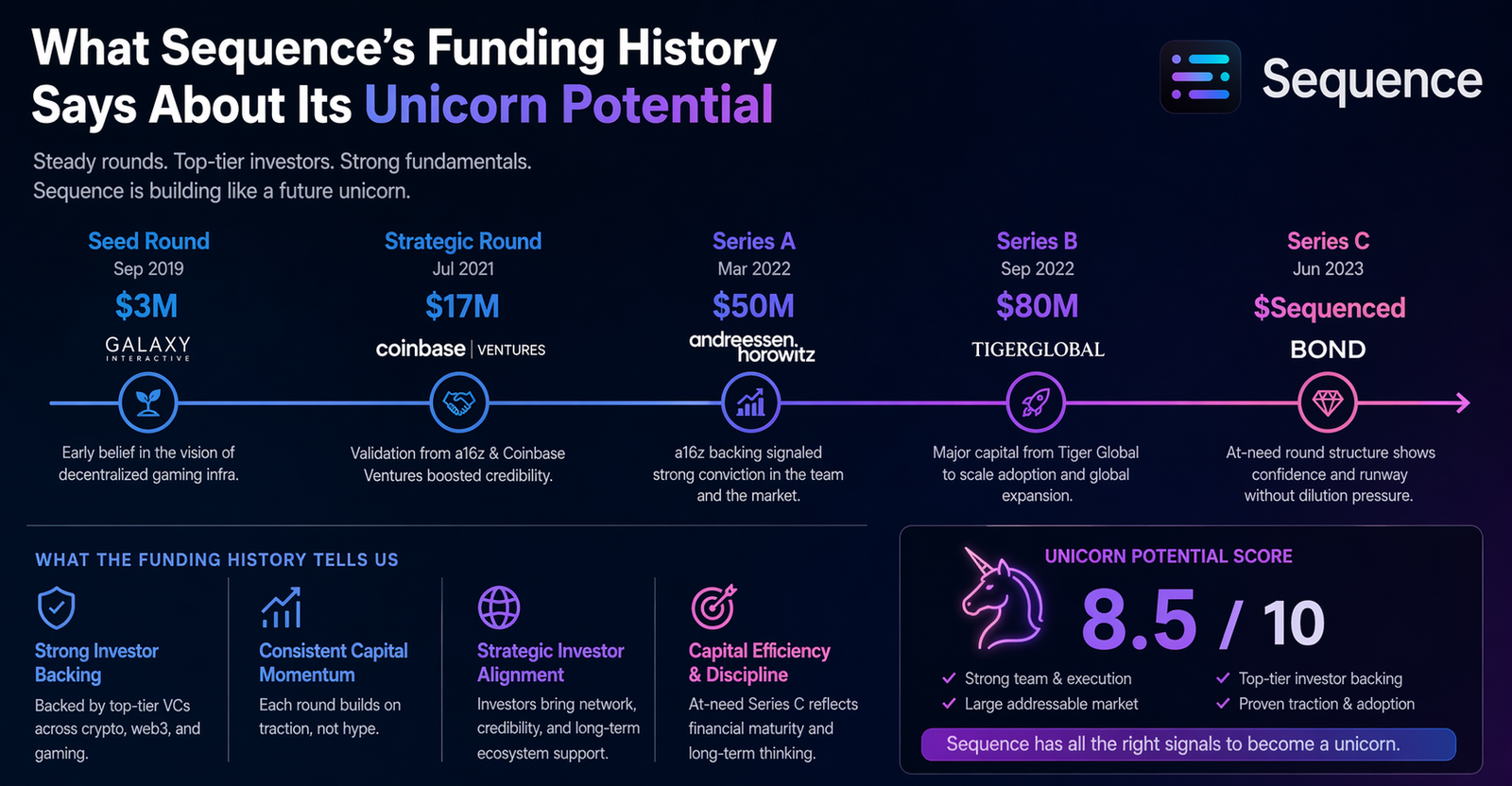

A lot of startups attract attention after a big funding round. Fewer create the kind of curiosity that makes people ask a very specific question: is this company already a unicorn, or is it getting close? That is where Sequence sits right now.

If you look at the publicly available funding record, the clearest answer is this: Sequence has strong momentum, but there is no public evidence in the sources available today that confirms a $1 billion valuation. Crunchbase defines a unicorn as a private company valued at $1 billion or more in a disclosed funding round, and that is an important distinction here. Sequence has announced meaningful rounds and impressive growth metrics, but it has not publicly disclosed a unicorn-level valuation.

That does not make the company any less interesting. In some ways, it makes the story more useful. Instead of forcing the label too early, Sequence’s funding history gives a better view of how investors are thinking about the business, what kind of traction the company is showing, and why people have started putting it in unicorn-adjacent conversations.

Sequence started with a seed round that got people’s attention

The first reason people take Sequence seriously is that the company did not begin with a quiet little raise. In September 2022, Sifted reported that Sequence raised a $19 million seed round led by Andreessen Horowitz, also known as a16z. Sifted said that round gave the company a $75 million post-money valuation, which is a notable number for a seed-stage startup in fintech and revenue software.

At the same time, the early valuation story came with a bit of noise. A TechCrunch report from that same period said earlier reports had pegged Sequence’s valuation in the $50 million to $60 million range, while also noting that Riya Grover said the startup would not be disclosing the number directly. That matters because it shows something important about the company’s funding history: even early on, Sequence was attracting enough investor demand to spark valuation speculation.

That is usually a sign that investors see more than a nice product demo. They see a bigger category opportunity. In Sequence’s case, that category is revenue operations, especially the messy work around billing, invoicing, collections, and revenue recognition. Those are not flashy problems on the surface, but they are painful, expensive, and deeply tied to how software and fintech companies actually make money.

The Series A made the bull case stronger

If the seed round put Sequence on the map, the Series A made the company harder to ignore. In December 2025, Sequence announced a $20 million Series A led by 645 Ventures, with participation from a16z, Firstminute Capital, Vor Capital, Passion Capital, and Dig Ventures. The company said the round brought total funding to $38 million.

That update mattered for more than the dollar amount. Sequence also said it had achieved 10x ARR growth that year and was working with finance teams at companies including Cognition, Legora, Bridge, 11x, incident.io, Runway, and Moonpay. In other words, the company was not just selling a vision. It was showing revenue growth, adoption, and recognizable customers.

A separate report from FF News reinforced the same picture. It described the Series A as coming after a year of 10x ARR growth and said that Sequence was being adopted by mid-market and enterprise companies to automate revenue operations. That kind of follow-up coverage matters because it suggests the company’s traction story is not limited to one self-published announcement.

Why investors are leaning in

When you step back, the attraction becomes easier to understand. Sequence is operating in a part of the software stack that still has a lot of manual work. In its own funding announcement, the company described finance and revenue teams as still relying on spreadsheets, fragmented tools, and manual processes for pricing, billing, collections, and revenue recognition. Riya Grover framed the problem as finance teams choosing between drowning in manual billing work or relying on systems that break under custom deals.

That is the kind of pitch investors like when it is backed by real usage. It is not just an AI wrapper chasing hype. It is software aimed at a real workflow with direct revenue consequences. The category language around quote-to-cash, contract-to-cash, billing automation, invoice automation, and finance-grade AI agents gives Sequence a clearer commercial story than many younger AI startups have.

There is also the market backdrop. Crunchbase News reported that AI and AI infrastructure were major drivers of new unicorn creation in early 2026, while TechCrunch reported that more than 100 tech startups reached unicorn status in 2025, with AI dominating the list. That does not prove anything about Sequence by itself, but it does explain why investors and readers are more willing to ask the question in the first place.

The strongest argument for Sequence’s unicorn potential is traction, not hype

This is the part that matters most. Unicorn potential is not only about how much money a company has raised. It is about whether its trajectory looks steep enough to support a future billion-dollar round.

On that front, Sequence has a few strong signals. The company says it posted 10x ARR growth in 2025. It says it is serving hundreds of finance teams. FF News adds that the platform is automating revenue operations for fast-growing businesses, and Riya Grover’s LinkedIn announcement said Sequence now automates over $1 billion in annual invoice volume. Those are the kinds of numbers that make later-stage investors pay attention.

Just as important, the customer profile fits the story. Companies like Cognition, incident.io, Bridge, Runway, and Moonpay are the kind of names that help a startup look more credible in enterprise software and fintech circles. A startup can have a clever product, but if the customer base is thin, investors notice. In Sequence’s case, the public story is leaning in the opposite direction. It suggests the company is finding real demand in a segment where automation can save time and reduce revenue leakage.

That is why the company feels closer to a serious scale-up than a speculative AI newcomer. The funding history points to consistent investor confidence, and the operating story gives that confidence something to stand on.

What is still missing from the unicorn case

Even with all that momentum, there is still a gap between a promising growth company and a confirmed unicorn. The missing piece is public valuation evidence.

Right now, the strongest clearly reported valuation tied to Sequence is the $75 million post-money figure reported by Sifted for the 2022 seed round. The later Series A announcement disclosed the amount raised, investors, and growth metrics, but not a new valuation. And because Crunchbase bases its unicorn board on valuations set in disclosed funding rounds, the absence of a public billion-dollar mark matters.

That is why the most honest reading is not “Sequence is already a unicorn.” It is “Sequence has some of the ingredients investors look for in a future unicorn, but the public record does not yet confirm that status.” That difference may sound small, but it is the difference between analysis and hype.

So, is Sequence a unicorn?

Based on the public information available now, no confirmed source shows Sequence at a $1 billion valuation. What the company does have is a strong early funding story, serious backers, a meaningful Series A, fast revenue growth, and a product aimed at a part of the finance stack that is still ripe for automation.That makes Sequence worth watching, even if the unicorn label is still premature. Its funding history tells a more grounded story than the headline question alone suggests. Investors have been willing to back Sequence from an unusually strong seed round into a larger growth round because they appear to believe the company is solving a painful, valuable, and scalable problem. Whether that turns into a public unicorn valuation later will depend on how fast Sequence keeps growing and what valuation the market is willing to attach to that growth in its next priced round.