If you are new to fundraising, the world of startup funding can feel much more complicated than it really is. Founders hear terms like pre-seed, Series A, valuation, and equity dilution, then suddenly every conversation sounds like it is happening in a different language. But once you break it down, most funding rounds follow a simple logic. Startups raise money in stages, and each stage comes with a different set of expectations from investors.

At its core, a funding round is a checkpoint. A startup raises capital to reach its next milestone, not to solve every future problem at once. In the early days, that money may go toward product development, building a prototype, hiring a small team, or proving there is a real market. Later rounds are usually about scaling, growing revenue, expanding into new markets, and building a stronger operating engine. That is why the type of investor changes as the company matures.

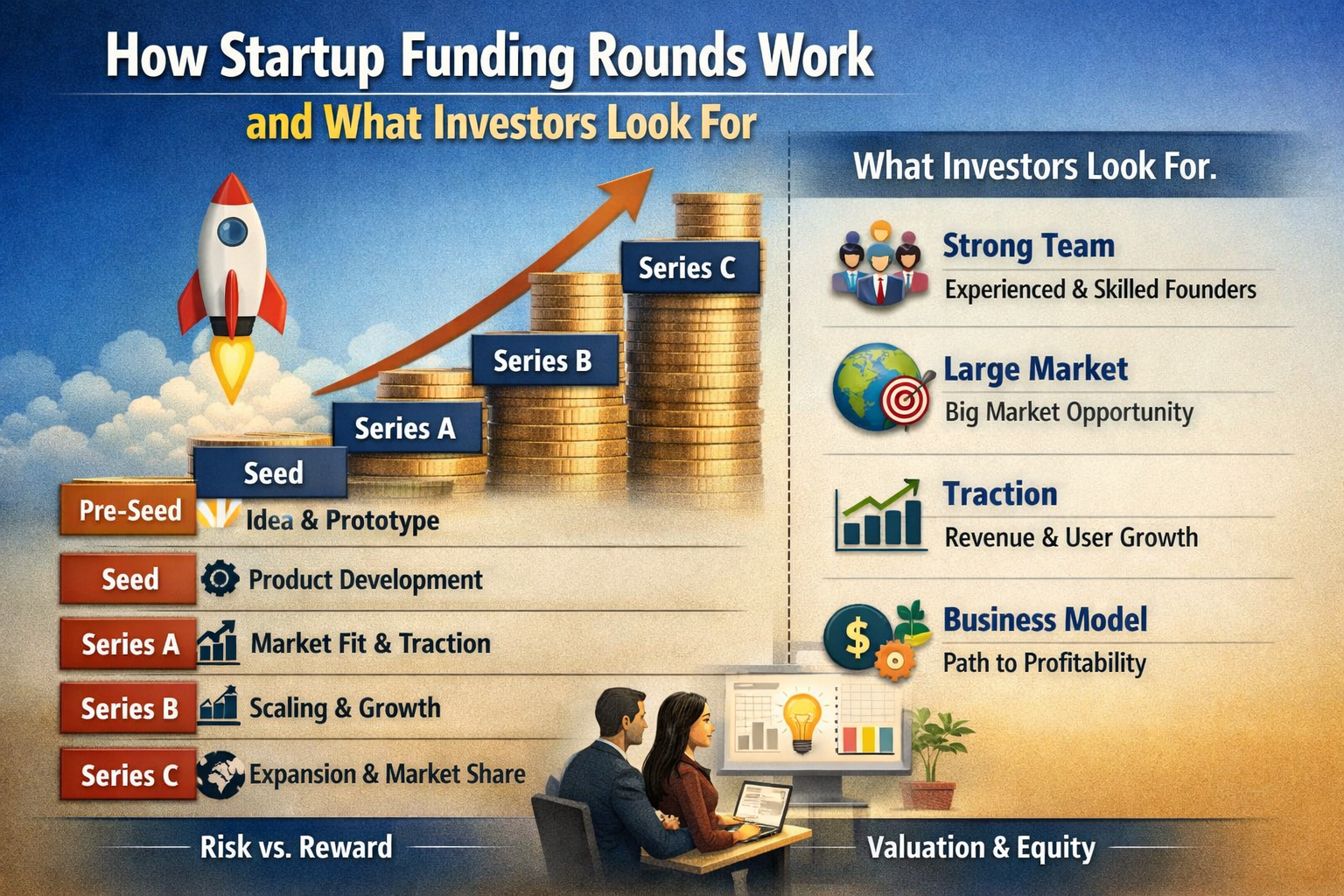

Why startups raise money in rounds

Most startups do not raise one giant amount of money on day one. Instead, they raise capital in steps because the business itself changes in steps. At the idea stage, there is not much proof yet, so investors are mostly backing the founding team, the market opportunity, and the founder’s ability to execute. Once the company has early traction, a product people actually use, and some real customer demand, investors begin to focus more on growth, efficiency, and whether the business can scale.

This staged approach helps both sides. Founders get the money they need to hit the next target, and investors get a chance to evaluate the company with more evidence at each round. It also reflects how startup risk changes over time. Early on, even technical feasibility and economic efficiency may still be uncertain. As the company progresses, the risk can go down while the amount of capital required goes up.

Pre-seed is mostly a bet on the founders

The pre-seed stage is usually the first meaningful outside raise. At this point, the company may still be little more than an idea, a rough prototype, or a very early product. Revenue is usually nonexistent or extremely small, which means investors are not backing a polished business yet. They are backing people. They want to see a strong founding team, a real problem worth solving, a market with room for growth, and a believable next step.

That is why pre-seed funding often comes from friends and family, angel investors, and startup programs like Y Combinator or Techstars. These early backers know the risk is high. What they care about is whether the founders have enough skill, focus, and determination to turn a rough idea into something real. In practical terms, the money is often used to validate the concept, build the product, and reach first users or first paying customers.

Seed funding is where the idea has to start acting like a business

By the time a startup reaches seed funding, the conversation changes. A great story is still helpful, but now investors want signs that the market is responding. That could mean a working product, early customer interest, some revenue, or enough momentum to suggest there is a path toward product-market fit. Seed capital is often used to sharpen the product, hire more people, improve operations, and test early growth channels.

At this stage, you will often see a mix of angel investors, early-stage venture capital firms, and sometimes accelerator networks or small funds. These investors are looking for traction, early validation, and a clear explanation of what the company will do with the money. They do not expect perfection. They do expect progress. A founder who can clearly explain the problem, the customer, and the next milestone usually has a much stronger fundraising story than someone who relies on hype alone.

Series A is where scalability becomes the big question

A lot of founders treat Series A as just a larger seed round, but that usually misses the point. Seed is about proving people care. Series A is about proving the business can scale. Investors at this stage want stronger evidence that growth is not random. They look at things like customer acquisition costs, retention, engagement rates, and whether the company has a real go-to-market strategy that can be repeated.

This is also the stage where the investor mix shifts toward more formal capital. Institutional investors and established venture capital firms lead many Series A rounds, with some participation from corporate venture arms, super angels, and micro-VCs. The bar is higher because the check sizes are higher. Investors want real proof that the startup is more than an interesting product. They want to see a path to becoming a real company with durable momentum.

Many of these investors expect meaningful growth signals by this point. Some startups entering Series A are already generating around $1M ARR, while others show strong engagement, retention, or user growth that supports the same basic argument. The exact number matters less than the pattern. Investors want to see that the startup has found something that works and can now turn that early traction into a repeatable growth engine.

Series B and later rounds are about scale, efficiency, and position

Once a company gets into Series B and later rounds, the story becomes less about early validation and more about execution at scale. By then, the startup should have a stronger business model, more predictable revenue, and a growing customer base. The company is no longer trying to prove it deserves a place in the market. It is trying to expand its share of that market and move faster than competitors.

That is why later-stage capital often goes toward market expansion, bigger teams, new product lines, infrastructure, and aggressive customer growth. Investors in these rounds care a lot about efficiency, revenue quality, and how large the company can realistically become. By the time startups reach Series C, investors are usually looking for much lower risk and much clearer returns. According to Digits, companies at that stage often show very high and more predictable revenue compared with earlier rounds.

What investors really look for at every stage

Even though the details change by stage, there are a few themes that show up almost every time. Investors want to back a strong team, a real market, and a company that knows how to use capital well. They want a founder who understands the customer, understands the market, and understands what milestone this round is supposed to unlock. In other words, investors rarely write checks just because the idea sounds exciting. They write checks when the story and the evidence line up.

This is where basics like a strong pitch deck, a solid business plan, and a clear use of funds become important. Founders need to explain the problem, the solution, the market, the business model, and the growth path without sounding vague or inflated. They also need to show why they are the right team to do it. Investors may forgive what is still unfinished. They are much less forgiving when the founder cannot explain the business clearly.

Valuation matters more than many first-time founders expect

One of the biggest mistakes founders make is focusing only on closing the round. Money feels like the win, but the structure of the deal matters too. Valuation shapes how much equity founders give up, how future rounds may look, and how much room there is for later fundraising. Give away too much too early, and the long-term cost can be painful. Raise at a valuation that is too aggressive, and the next round may become much harder if growth does not keep up.

This matters even more in a market where valuations can shift. Crunchbase News notes that startups returning to the market after long funding gaps sometimes raise at unclear or reduced valuations, and some may accept a valuation cut to secure fresh financing. That does not mean the company is doomed. It simply shows that fundraising is not just about the company itself. It is also shaped by timing, market conditions, and investor sentiment.

A big round does not always mean a healthy business

This is the part many fundraising articles skip. Raising money is important, but it is not proof that everything is working. Sometimes the market rewards momentum for a while, then later forces a reset. A company can raise large sums, gain attention, and still run into operational, manufacturing, or strategy problems that money alone cannot fix.

The Monarch Tractor story is a good example. TechCrunch reports that the company raised more than $200 million over eight years, but later struggled, lost its manufacturing path after Foxconn sold the plant that had been producing its tractors, and eventually saw its assets acquired by Caterpillar. For founders, the lesson is simple. Capital is fuel. It is not the same thing as stability, product strength, or a repeatable business.

How founders should prepare before talking to investors

Before reaching out to investors, it helps to answer three questions clearly. What milestone are you raising for? What proof do you already have? Why is this the right type of investor for your company? If you cannot answer those questions cleanly, fundraising will feel scattered. If you can, the whole process becomes much more focused.

A strong fundraising setup usually includes a sharp pitch deck, a realistic growth story, a clear explanation of the market, and specific numbers around product usage or revenue where possible. It also helps to know what kind of help you want from investors beyond the money. Some bring distribution, some bring hiring support, some bring introductions, and some mainly bring a check. The right investor is not just someone willing to fund the round. It is someone who fits the company’s stage and direction.

Founders should also remember that investor relationships start before the term sheet. Good fundraising is often built on clarity, consistency, and trust. If your story changes every meeting, the market definition is fuzzy, or the use of funds is vague, investors will notice. If your message is sharp and the proof is real, you immediately stand out more. That matters in a crowded startup ecosystem where investors are constantly comparing companies side by side.

The simple way to think about startup funding rounds

The easiest way to understand startup funding rounds is to stop seeing them as labels and start seeing them as milestones. Pre-seed is about belief in the founders. Seed is about early proof. Series A is about scalable growth. Series B and later are about expansion, efficiency, and market position. Investors look for different things at each step, but the underlying question stays the same: has this company earned the right to raise the next round?

If founders understand that, fundraising becomes much less mysterious. It becomes a matter of matching the right evidence to the right stage, choosing investors who fit the business, and raising enough capital to reach the next milestone without losing sight of the bigger picture. That is usually what separates a smart raise from a rushed one.